日本語|English (current)

On December 29, 1989, the Nikkei 225 closed at 38,915.87, the best-known peak of Japan’s asset-price bubble. In hindsight, the number looks like a warning sign. At the time, however, strong Japanese manufacturers, rapid corporate investment, Tokyo’s rising role as a financial center, and the apparent scarcity of urban land offered explanations that made high prices seem plausible.

-

- 東京証券取引所ビル。建物は1988年完成、写真は2018年撮影。Kakidai/Wikimedia Commons/CC BY-SA 4.0。

The Tokyo Stock Exchange building, completed in 1988. The photograph was taken in 2018. Kakidai / Wikimedia Commons / CC BY-SA 4.0. This is not a photograph of the exchange floor or the final trading day of 1989.

Japan’s bubble did not arise from one policy, and it did not collapse in a single moment. Financial liberalization changed banks’ business models. The Plaza Accord accelerated yen appreciation. Monetary easing supported domestic demand. Land collateral, equity finance, cross-shareholdings, tax and planning rules, and optimistic expectations reinforced one another. After the turn, losses moved from shares to land, borrowers, banks, credit supply, business investment, employment, and deflation. The cleanup lasted into the 2000s.

- The conclusion first: there was no single cause

- A timeline from the boom to the cleanup

- Before the bubble: a bank-centered financial system

- The Plaza Accord and the rapid rise of the yen

- Why monetary easing lasted

- How land, shares, and credit reinforced one another

- Late Shōwa optimism—and its limits

- The turning point: rate increases and the lending restriction

- The collapse was a sequence, not a date

- Why bad-loan disposal was delayed

- The jusen crisis

- The 1997–1998 financial crisis

- Credit contraction, employment, and the employment ice age

- Deflation and the balance-sheet recession

- The cleanup in the 2000s

- Who was responsible?

- Testing common claims

- Conclusion

- References

The conclusion first: there was no single cause

- International setting: the United States sought an adjustment of an overvalued dollar and large external imbalances, leading to the 1985 Plaza Accord among the G5.

- Domestic response: Japan used monetary easing and measures to expand domestic demand as the yen rose and exporters weakened.

- Financial transformation: large corporations gained easier access to bond and equity markets, while banks searched for new borrowers in real estate, small business, nonbanks, and households.

- Collateral feedback: rising land prices increased collateral values, which supported more lending and further purchases of land, shares, and development projects.

- Delayed recognition: weak disclosure standards, hopes for a land-price recovery, thin bank capital, accounting constraints, and political resistance to public support slowed the disposal of bad loans.

A timeline from the boom to the cleanup

| Date | Event | Why it mattered |

|---|---|---|

| September 22, 1985 | Plaza Accord | The G5 endorsed policy coordination and an orderly adjustment of the dollar. |

| January 1986–February 1987 | Official discount rate cut from 5% to 2.5% | Support for the economy after rapid yen appreciation. |

| 1987–1989 | Rapid growth in asset prices and credit | Land-backed lending, zaitech, and equity finance expanded. |

| May 1989 | Bank of Japan began raising rates | The official discount rate eventually reached 6% in August 1990. |

| December 29, 1989 | Nikkei 225 closed at 38,915.87 | The historical equity-market peak. |

| March 1990 | Quantitative restriction on real-estate lending | Banks were told to keep growth in real-estate loans below total loan growth. |

| 1990–1992 | Shares fell, then land weakened | Collateral values declined and non-performing loans increased. |

| 1995–1996 | Jusen settlement | A ¥685 billion fiscal contribution caused intense controversy. |

| November 1997 | Major failures including Hokkaido Takushoku Bank and Yamaichi Securities | Systemic distrust became visible. |

| 1998 | LTCB and NCB placed under temporary public control | Resolution, supervision, and recapitalization frameworks were strengthened. |

| October 2002 | Program for Financial Revival | Asset assessment and NPL disposal accelerated. |

| March 2005 | Major-bank NPL ratio fell to 2.9% | Down from 8.4% in March 2002. |

Before the bubble: a bank-centered financial system

During the high-growth decades, Japanese firms relied heavily on bank loans. A main bank was the institution with the deepest long-term relationship with a company, supplying credit, monitoring management, and coordinating assistance during distress. The Bank of Japan also used window guidance(窓口指導), an administrative practice through which it influenced how much individual banks expanded lending.

The Ministry of Finance regulated interest rates, products, entry, and business boundaries. This broader framework later became known as the convoy system(護送船団方式): close official control combined with a preference for stability and avoidance of disorderly failure.

From the 1970s, bond markets, equity issuance, overseas borrowing, and market-based interest rates expanded. Large, highly rated corporations reduced their dependence on bank loans. Household deposits, however, continued to flow into banks. Financial institutions therefore sought new customers in property, small and medium-sized firms, households, and nonbank lenders. Not every loan was speculative; office demand and redevelopment were real. The danger arose when lending decisions depended more on rising collateral values than on cash flow.

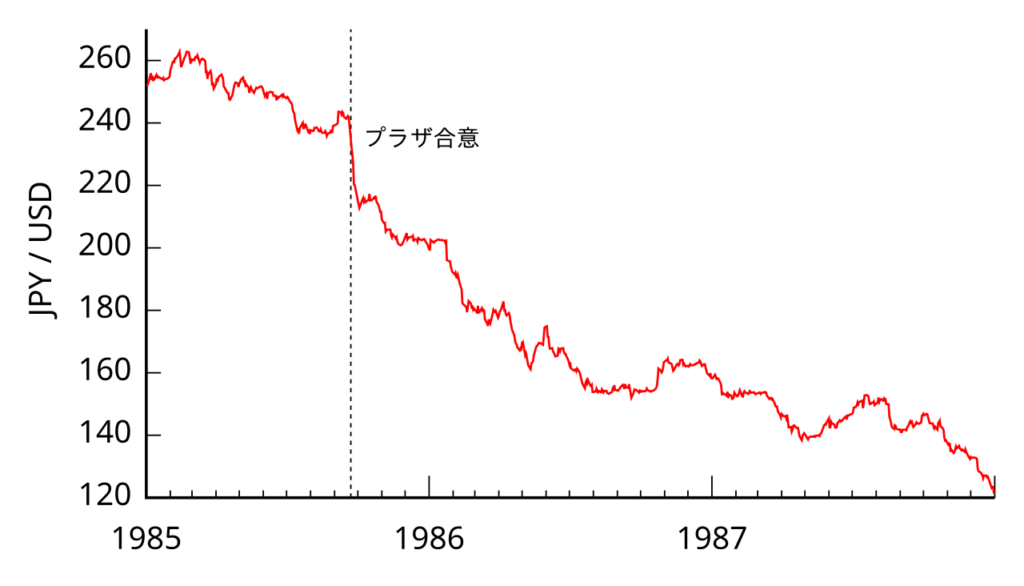

The Plaza Accord and the rapid rise of the yen

-

- 1985年から1987年末までの円ドル相場。点線は1985年9月22日のプラザ合意。Monaneko/Wikimedia Commons/CC BY 3.0。データ:Federal Reserve。

The U.S. dollar–Japanese yen exchange rate from 1985 through the end of 1987. The dotted line marks the Plaza Accord of September 22, 1985. The vertical axis is yen per dollar, so a lower number means a stronger yen. Monaneko / Wikimedia Commons / CC BY 3.0. Data: Federal Reserve.

The Plaza Accord was reached by the finance ministers and central bank governors of the United States, Japan, West Germany, France, and the United Kingdom. It reflected concern over the strong dollar and large international imbalances. The participants supported an orderly adjustment of exchange rates and greater policy coordination.

The yen appreciated from roughly ¥240 per dollar around the agreement toward the ¥120s by the end of 1987. Japanese exporters faced weaker yen-denominated earnings and pressure to move production abroad. The slowdown was widely described as the endaka fukyō, or “high-yen recession.”

The Accord mattered, but it did not mechanically create the bubble. It changed the international environment. Japan’s domestic choices—how long to ease, how to supervise banks, how to tax and regulate land, and how to respond to credit growth—shaped what followed.

Why monetary easing lasted

-

- 日本銀行本店。Fg2撮影/Wikimedia Commons/Public Domain。

The Bank of Japan’s head office. Fg2 / Wikimedia Commons / Public Domain. The image identifies the institution; it is not a photograph of a bubble-era policy meeting.

The official discount rate was the benchmark rate at which the Bank of Japan lent to financial institutions. Between January 1986 and February 1987, the Bank reduced it from 5% to 2.5% in five steps. The 2.5% rate remained until May 1989.

Several considerations supported this stance: the high-yen recession, international policy coordination, the government’s desire to expand domestic demand, relatively stable consumer prices, and concern after the global stock-market crash of October 1987.

The crucial distinction was between inflation in goods and services and inflation in asset prices. Consumer prices remained comparatively calm while land and shares surged. Within the policy framework of the time, weak consumer inflation was a reason not to tighten aggressively. In hindsight, the combined growth of credit, money, investment, land prices, and share prices signaled a dangerous financial imbalance.

How land, shares, and credit reinforced one another

In land-backed lending, property serves as security for a loan. When land prices rise, the apparent collateral value rises. That can support a larger loan, which can finance more land, shares, or development.

Higher land prices → higher collateral values → greater lending capacity → more purchases and investment → still higher asset prices

This is a simplified model. Actual land values also depended on rents, office demand, redevelopment, inheritance-tax planning, zoning, supply constraints, and local conditions. But when underwriting relied on the belief that land would not fall, a reversal produced losses far beyond the original transaction.

The shorthand for this expectation was the land myth(土地神話)—the belief that scarce Japanese land, especially in major cities, would retain or increase its value. It was not a formal doctrine and was not universally believed, but it influenced banks, companies, households, and policymakers.

Equity prices had a related but different mechanism. Japanese firms and banks held one another’s shares through extensive cross-shareholding. Rising prices created unrealized gains, or hidden reserves(含み益), and companies raised funds through shares, convertible bonds, and warrant bonds. Investment of corporate surplus funds in securities and property became known as zaitech(財テク). Land and equities influenced one another, but they did not peak at exactly the same time or move identically across regions and sectors.

Late Shōwa optimism—and its limits

The late Shōwa era, ending in January 1989, saw strong corporate hiring, expensive entertainment, purchases of overseas real estate and art, resort development, golf-membership speculation, and a growing role for corporate finance departments. Optimism drew strength from genuine facts: internationally competitive manufacturers, rapid investment, Tokyo’s rise as a financial center, and scarce urban land.

Yet “everyone became rich” is inaccurate. Many households did not own shares or investment property. Rising land prices made housing less affordable, especially for younger urban families. Benefits differed by region, age, occupation, and asset ownership.

The turning point: rate increases and the lending restriction

The Bank of Japan raised the official discount rate from 2.5% to 3.25% in May 1989 and eventually to 6% in August 1990. Share prices peaked at the end of 1989 and fell sharply in 1990.

In March 1990, the Ministry of Finance introduced the quantitative restriction on real-estate lending(不動産融資総量規制). Banks were instructed to keep the growth rate of loans to the real-estate industry below the growth rate of total lending.

Was the measure too late or too abrupt? Both arguments have evidence. It came after years of rapid credit growth and contained exceptions and indirect routes. Yet it also coincided with higher rates, tax changes, and a shift in expectations, tightening credit during a fragile adjustment. The policy did not destroy an otherwise sustainable market; neither did it provide a painless correction.

The collapse was a sequence, not a date

Falling share prices → falling land prices → lower collateral values → repayment problems → more non-performing loans → tighter bank credit → weaker investment, employment, and consumption

A non-performing loan is a loan whose repayment is doubtful because the borrower has failed, is seriously delinquent, or has received concessions such as reduced interest or extended maturity. Japan’s disclosure standards changed repeatedly during the 1990s, so rising reported totals reflected both deterioration and broader definitions.

Falling asset prices became systemic because companies, banks, nonbanks, and related firms were connected through loans, guarantees, collateral, and shareholdings. Losses that began in markets migrated into institutions that supplied everyday credit.

Why bad-loan disposal was delayed

Many banks and borrowers expected land prices to recover. Delaying foreclosure could therefore appear cheaper than recognizing a loss immediately. Banks also had incentives to avoid bankrupting clients: failure would crystallize losses and reduce bank capital. Additional loans, payment extensions, and interest concessions kept some firms alive but often postponed restructuring.

Accounting, tax, and supervisory systems were not designed for rapid recognition of market-based losses. Under the Basel capital framework, writing down loans and suffering share-price losses could reduce regulatory capital and force banks to shrink lending. Banks’ use of unrealized equity gains as part of capital made the decline in share prices especially damaging.

It is too broad to say that “the government knew everything and hid it.” Some institutions did conceal losses or rely on unrealistic recovery plans. But estimates also varied because collateral values, group-company exposure, restructured loans, and future cash flows were genuinely uncertain, while reporting definitions evolved.

The jusen crisis

Jusen housing-loan companies(住宅金融専門会社)were created in the 1970s to supplement mortgage finance. As parent banks moved directly into housing loans, the jusen increasingly financed property companies and development projects. Their funding came from parent banks and agricultural and forestry financial institutions, among others.

The 1990 real-estate lending restriction did not initially cover the jusen directly, allowing them to become one channel through which property credit continued. After the collapse, seven jusen accumulated enormous losses. In 1995–1996 the government designed a settlement including ¥685 billion in fiscal funds.

Public anger was intense because the measure appeared to use tax money to absorb losses created by banks, nonbanks, borrowers, and regulators without a clear allocation of responsibility. Yet disorderly failure also threatened lenders and financial confidence. The need to protect the system and the duty to impose losses and explain responsibility were separate questions.

The 1997–1998 financial crisis

Several shocks converged in 1997. The consumption tax rose from 3% to 5% in April. Household burdens from social insurance and medical costs increased, while public investment moved toward restraint. The Asian financial crisis spread from July. Domestic demand weakened, exports and confidence came under pressure, and doubts about banks intensified.

No single factor is sufficient. The tax increase reduced demand, but did not create the banks’ property losses. The Asian crisis hurt exports and confidence, but did not create the domestic bad loans. Fiscal choices, external shocks, and unresolved banking weakness interacted.

In November 1997, Sanyo Securities failed, Hokkaido Takushoku Bank collapsed, and Yamaichi Securities announced its closure. Sanyo’s default in the interbank market was especially damaging because it undermined confidence in short-term financial claims. Japanese banks also faced a “Japan premium” when borrowing dollars abroad.

-

- かつて山一證券本社が置かれた茅場町タワー。写真は2012年撮影。Harani0403/Wikimedia Commons/CC BY-SA 3.0。

Kayabacho Tower, once the location of Yamaichi Securities’ headquarters. Photograph taken in 2012. Harani0403 / Wikimedia Commons / CC BY-SA 3.0. It is not a photograph of the 1997 closure announcement.

In June 1998, the Financial Supervisory Agency began operations, separating major supervisory functions from the Ministry of Finance. The Long-Term Credit Bank of Japan was placed under temporary public control on October 23, 1998, and Nippon Credit Bank followed on December 13. Japan adopted stronger frameworks for resolution, nationalization, asset assessment, and recapitalization.

-

- 新生銀行旧本社ビル。旧日本長期信用銀行の後身にあたる新生銀行が使用した建物。写真は2006年撮影。Lombroso/Wikimedia Commons/Public Domain。

The former headquarters of Shinsei Bank, successor to the Long-Term Credit Bank of Japan. Photograph taken in 2006. Lombroso / Wikimedia Commons / Public Domain. It is not an image of the 1998 nationalization.

Credit contraction, employment, and the employment ice age

Credit crunch, or kashishiburi(貸し渋り), describes tighter standards for new loans and refinancing. Loan withdrawal, or kashihagashi(貸し剥がし), refers to aggressive reduction or recovery of existing credit. When banks tried to preserve capital ratios, even viable small and medium-sized firms could lose access to funds.

Businesses cut investment and recruitment. Bankruptcies and restructuring increased. The decline in graduate hiring was especially consequential because Japan’s synchronized recruitment of new graduates made the first job a major gateway to stable careers. Those entering the labor market in the worst years became known as the employment ice-age generation.

The Ministry of Health, Labour and Welfare reports that the effective job-offers-to-applicants ratio remained below one from 1993 through 2005, while unemployment reached 5.4% in 2002. Not every labor-market change came from the bubble collapse; demography, industrial restructuring, deregulation, and changing employment practices also mattered. Still, prolonged weak demand left a measurable generational scar.

Deflation and the balance-sheet recession

Deflation is a sustained decline in the general price level. It raises the real burden of debt because the face value of loans does not fall with prices. After property and share prices collapsed, firms often prioritized debt reduction over new investment. This is commonly called a balance-sheet recession.

When households, firms, and banks all try to repair balance sheets at once, economy-wide spending weakens. Low interest rates may not produce strong borrowing if companies already have excess debt and capacity. Japan used repeated monetary easing and fiscal packages, but recoveries were interrupted by yen appreciation, fiscal restraint, financial instability, and the Asian crisis.

The cleanup in the 2000s

From 1998 onward, Japan built a stronger resolution and supervisory structure: public recapitalization, stricter inspections, the Financial Inspection Manual, and the Resolution and Collection Corporation. In October 2002, the Program for Financial Revival called for tougher asset assessment and aimed to roughly halve the non-performing-loan ratio of major banks by fiscal 2004.

According to the Financial Services Agency, the major-bank NPL ratio fell from 8.4% in March 2002 to 2.9% in March 2005. This marked normalization of the acute banking problem, not the disappearance of every consequence. Deflation expectations, damaged careers, regional banking problems, corporate restructuring, and public debt remained.

Who was responsible?

| Actor | What it did | What was later criticized |

|---|---|---|

| G5 and international policy | Coordinated adjustment of the dollar | Pressure toward yen appreciation, but no direct control over Japan’s land and banking rules. |

| Japanese government and Ministry of Finance | Expanded domestic demand, liberalized finance, supervised banks, regulated property lending | Slow disclosure and supervision, timing and design of restrictions, weak explanation of loss allocation. |

| Bank of Japan | Eased after the high-yen recession, later tightened, then eased after the collapse | Length of low rates, attention to asset and credit growth, speed of post-collapse easing. |

| Banks, nonbanks, and jusen | Expanded property and collateral-based lending | Concentration risk, weak underwriting, delayed loss recognition, governance failures. |

| Securities firms and corporations | Expanded equity finance, cross-shareholding, and zaitech | Dependence on rising prices and inadequate loss disclosure. |

| Property firms and investors | Developed and traded land and speculative assets | Leverage and extrapolation of rising prices; participation was never universal. |

Testing common claims

“The Plaza Accord destroyed Japan.”

Supported: it accelerated yen appreciation and strongly shaped Japan’s domestic response.

Oversimplified: bank behavior, land rules, collateral lending, and delayed loss recognition were domestic mechanisms.

Still debated: how constrained Japan was by international coordination and whether its response was proportionate.

“Low interest rates alone created the bubble, and the Bank of Japan burst it.”

Supported: easy money supported credit and asset demand; tightening changed expectations.

Oversimplified: regulation, taxation, financial liberalization, cross-shareholding, and collateral practices amplified the boom.

Still debated: when tightening should have begun and how fast easing should have resumed.

“Public money only rescued bank executives.”

Supported: unclear burden-sharing and weak accountability deserved criticism.

Oversimplified: disorderly failures could destroy deposits, payments, credit, firms, and jobs.

Still debated: the timing, amount, and allocation of losses among shareholders, managers, creditors, and taxpayers.

Conclusion

Japan’s bubble emerged from the interaction of international monetary adjustment, prolonged easing, financial liberalization, bank competition, land-collateral lending, equity finance, urban and tax institutions, and widely shared expectations. Its collapse moved in stages—from shares to land, from collateral to bad loans, from bank weakness to credit contraction, and from corporate retrenchment to employment and deflation.

The central lesson is not simply “avoid low rates” or “never use public money.” Stable consumer prices can coexist with dangerous financial imbalances. Collateral values can magnify both expansion and contraction. Delaying recognition of losses may increase the eventual social cost. Historical judgment also requires discipline: what actors could see at the time must be distinguished from what became obvious only after the crisis.

日本語|English (current)

References

- Japan Exchange Group, JPX Report 2021.

- U.S. Department of the Treasury, Exchange Stabilization Fund History.

- Okina, Shirakawa and Shiratsuka, Japan’s Experience in the Late 1980s and the Lessons.

- Shigenori Shiratsuka, Asset Price Bubble in Japan in the 1980s.

- Bank of Japan IMES, Japan’s Experience of Financial Liberalization.

- Policy Research Institute for Land, Infrastructure, Transport and Tourism, research on land-price formation.

- Financial Services Agency, report on failed financial institutions.

- Deposit Insurance Corporation of Japan, research on the jusen resolution.

- International Monetary Fund, Japan’s Economic Crisis and Policy Options, 1998.

- Financial Services Agency, Normalization of the NPL Problems of Major Banks, 2005.

- Ministry of Health, Labour and Welfare, 2024 Analysis of the Labour Economy.

Accessed July 16, 2026. Figures are used only where definitions and institutional coverage are sufficiently clear; different official series are not forced into a single total.